Unlocking Opportunity: Navigating the 5/1 ARM Loan

If you're seeking a lower monthly payment and anticipate a short stay in your home, a 5/1 adjustable-rate mortgage (ARM) loan might be a viable option. Typically, during the initial five years, 5/1 ARMs offer lower rates compared to 30-year fixed-rate mortgages. It's crucial to grasp how the rate adjusts after this initial period to determine if the initial lower payment justifies it.

What is a 5/1 ARM Loan?

A 5/1 ARM, short for 5-year Adjustable Rate Mortgage, offers a fixed interest rate for the initial

five years of the loan term, followed by potential adjustments based on prevailing market conditions. This type of mortgage is often referred to as a "hybrid mortgage" because it combines a fixed-rate period with subsequent variable-rate adjustments.

During the first five years, borrowers enjoy stability with a fixed interest rate. After this period, the rate can fluctuate annually based on predetermined terms. The "5" signifies the duration of the initial fixed-rate period, while the "1" indicates the frequency of rate adjustments thereafter, occurring annually.

How does a 5/1 ARM work?

During the initial fixed-rate period, borrowers typically benefit from a lower rate, often referred to as the "introductory rate." Following this period, the rate may fluctuate based on six key factors:

- Initial adjustment cap: This cap limits how much the interest rate can increase once the fixed-rate period ends. Typically set at 2% or 5%, it ensures that the new rate cannot rise by more than 2 or 5 percentage points initially.

- Adjustment period: The frequency of rate adjustments is determined by the adjustment period. For instance, a 5/1 ARM adjusts annually after the initial five-year fixed-rate period. Adjustment periods can range from monthly to every five years.

- Periodic cap: This cap restricts the maximum increase in the interest rate during each adjustment period after the initial one.

- Index: An index serves as a benchmark variable rate influenced by market and economic conditions. Lenders add a margin to the index to determine the borrower's rate during each adjustment period. Lenders should offer clear information on how the selected index has fluctuated over time.

- Margin: The margin is a fixed number determined by the lender. It is added to the index to calculate the borrower's rate when adjustments occur.

- Lifetime cap: Many ARMs come with a lifetime cap, often set at 5%. This cap ensures that the borrower's rate can never exceed a certain percentage, usually 5 points higher than the initial rate.

Interest-only ARMs: What are they and how do they work?

Certain 5/1 ARM programs offer an interest-only option, enabling eligible borrowers to pay solely the interest portion of the loan for a specified period, typically spanning from three to 10 years. Opting for this feature could be advantageous for borrowers aiming to minimize their monthly payments temporarily. However, it's essential to note that during the interest-only period, the loan principal remains untouched. Consequently, when this period ends, borrowers may experience a significant increase in their payments if the loan balance has not been reduced.

When a 5/1 ARM’s Interest Rate Adjusts

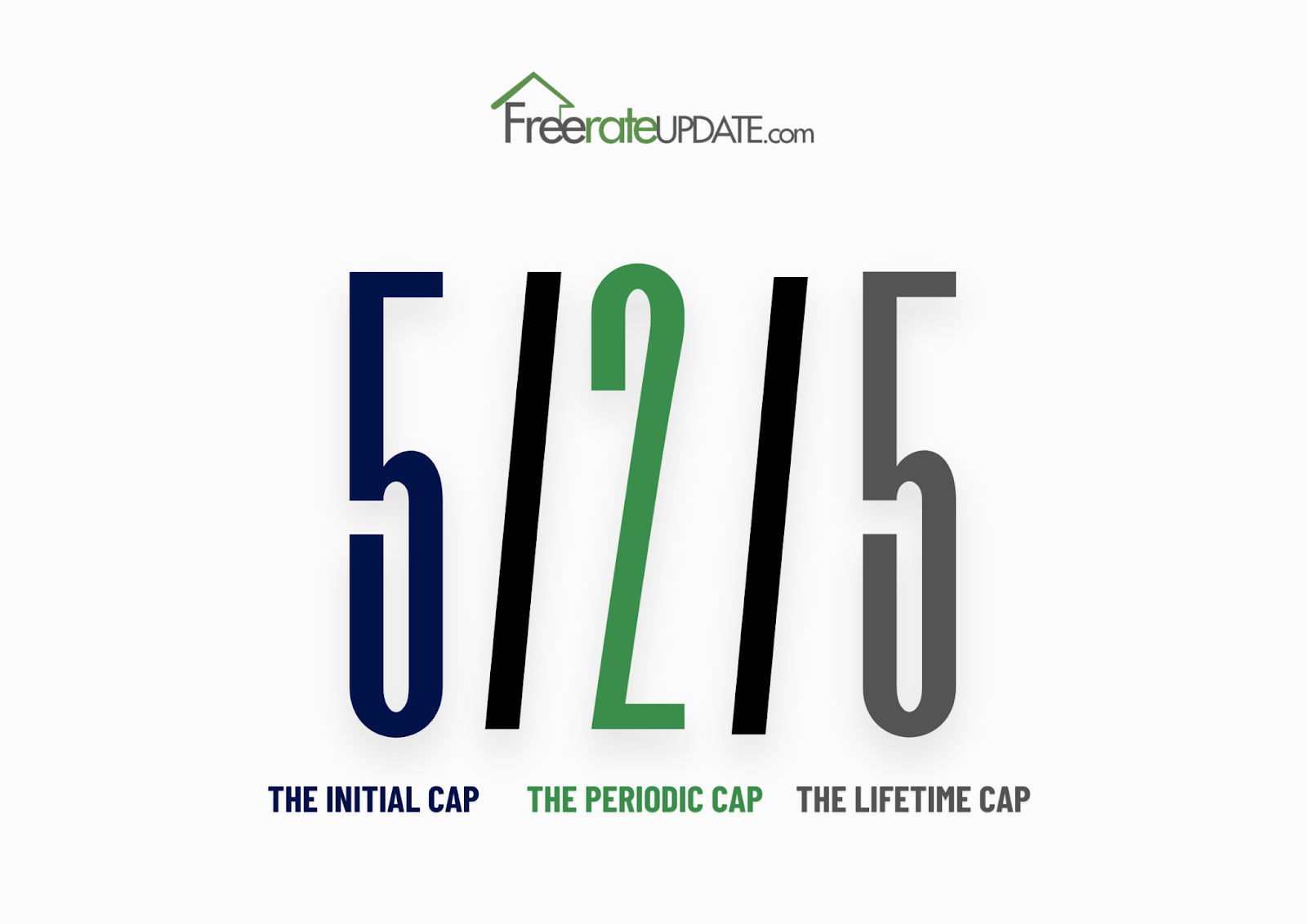

Understanding when a 5/1 ARM adjusts involves grasping how each "cap" is disclosed. When reviewing ARM details, you might encounter caps presented as a sequence of three numbers.

For example, an ARM with a "2/1/5 cap" signifies the following:

The initial cap: This indicates that your rate can increase by a maximum of 2 percentage points during the first adjustment period.

The periodic cap: This denotes that your rate can increase by up to 1 percentage point with each subsequent adjustment after the initial one.

The lifetime cap: This indicates that your rate can adjust by a maximum of 5 percentage points above the initial rate throughout the loan's duration.

When a 5/1 ARM’s Interest Rate Adjusts

Understanding the index is crucial as it represents the dynamic component of your adjustable rate, fluctuating in response to market shifts. Your lender selects the index to be utilized, with common choices including the Cost of Funds Index (COFI) or the one-year Constant Maturity Treasury (CMT) securities index.

You might encounter the term "fully indexed," which simply indicates the combined rate when your margin and index are added together. To calculate your fully indexed rate, you sum the current index rate with your margin. For instance, if the CMT index rate presently stands at 2%, and your margin is 5%, your fully indexed rate would amount to 7%.

5/1 ARM loan payment example

Upon applying for an ARM, you'll be furnished with a comprehensive 13-page Consumer Handbook on Adjustable-Rate Mortgages (CHARM) disclosure booklet along with a loan estimate elucidating the potential fluctuations in your rate and payment over time. This booklet serves as a valuable resource to enhance your understanding of the applied-for loan.

As an illustrative scenario, consider a 5/1 ARM with 2/2/5 caps. For instance, if you're borrowing $300,000 with an initial rate of 4.5%, here's a hypothetical breakdown of how the loan could adjust:

Initial Rate: 4.5%

Initial Cap: 2%

Subsequent Adjustment Cap: 2%

Lifetime Cap: 5%

This example offers insight into the potential adjustments your ARM could undergo, facilitating a clearer comprehension of your loan terms and potential future payments.

If you fail to refinance to a fixed rate before your ARM resets, you might face an additional $300 per month on your mortgage payment after the first adjustment. In the worst-case scenario, your monthly payment could surge by $500.

Pros and Cons of 5/1 ARM

While ARM rates can initially be lighter on your finances, they pose long-term risks. Familiarizing yourself with the pros and cons of a 5/1 ARM will empower you to make a well-informed decision.

Is a 5/1 ARM a Good Idea?

The potential risk of an ARM lies in the potential for rapid escalation in your monthly payments if interest rates spike. However, with a carefully crafted plan aligned with the specifics of your ARM, such concerns can be mitigated. The prospect of your ARM adjusting to significantly higher interest rates shouldn't instill fear, provided that you've ensured the suitability of the ARM for your lifestyle and financial circumstances.

You should consider a 5/1 ARM if:

- Plan to sell or refinance before the fixed-rate period expires. Timing a sale precisely with an impending ARM adjustment can be challenging. Allow ample lead time to market your home, or prepare your budget for the potential increase in the first payment adjustment.

- Consider anticipated income growth. If you expect a raise or bonus, payment increases may be less concerning as you'll have the resources to quickly pay down your loan's principal balance if needed.

- Opt for a higher down payment. A lower loan amount and monthly payment can cushion the impact if you're unable to pay off an ARM loan before it adjusts.

- Ensure you can afford the fully indexed payment. For instance, in the given example, there's a payment increase of over $1,000 if you end up with an ARM longer than anticipated. Avoid selecting an ARM if the higher payment would strain your budget.

Is Now a Good Time to Consider an ARM?

The interest in ARMs surged notably when mortgage rates began rising in 2021. On the LendingTree platform, borrowers were presented with ARM options more than three times as often in the first half of 2022 compared to the same period in 2021.

Up until the middle of 2022, ARMs consistently boasted lower interest rates than comparable fixed-rate mortgages, with a substantial average difference of 89 basis points. This translated into potential monthly savings of about $157 for borrowers opting for an ARM over a fixed-rate loan.

However, by early 2023, the gap between ARMs and 30-year fixed-rate mortgages had significantly narrowed. It's crucial to conduct thorough comparisons of loan offers before finalizing a decision. While ARMs have historically offered potential savings, they're not guaranteed to be the most cost-effective option. Factors such as current market conditions, individual financial situations, and future interest rate projections should be carefully considered before opting for an ARM.

5/1 ARM vs. Fixed-Rate

While many homeowners favor the predictability of a 30-year fixed-rate mortgage payment throughout the loan term, opting for a 5/1 ARM rate might be prudent, particularly when current 30-year mortgage rates are elevated. This choice is particularly appealing if you anticipate relocating within five years. Consider allocating the savings from a five-year ARM payment toward a dedicated moving expense account.

Here's a comparative analysis of the characteristics of a fixed-rate mortgage versus a 5/1 ARM: